After decades of being confined to history books at least for the Western world, inflation has been making a comeback for the last few quarters.

It started with the rally in commodities, especially oil and metals, post Covid in 2020 after a 10-15 year period when various commodity prices had remained largely subdued.

After some ups and downs in 2021, the prices started to accelerate around the beginning of the New Year. Added to this cyclical upturn have been climate events impacting agriculture produce; supply disruptions thanks to the pandemic and so on - all of which have contributed to an upward pressure on prices.

In the US and some other developed economies, housing prices have also been on a run as many government policies to help the citizens over the hump of the pandemic resulted in excess liquidity for households, especially as spending options were limited thanks to the pandemic. This liquidity was partly used for real estate purchases. Therefore, many components of the consumption/ inflation basket had been seeing rising prices over the second half of 2021.

Several central banks assessed that the supply constraint causing part of this inflation would ease over time and the inflation would prove to be transitory. This proved to be more of a hope than anything else, with inflation continuing to persist.

These trends accelerated with the rising Russia Ukraine tensions early in this year culminating in a full-fledged war by the end of February. Even before the actual war on the ground, prices of a whole lot of commodities from crude oil and natural gas to aluminum, palladium, nickel, potash to wheat & edible oils had already risen 20 to 30% since January 1.

This has only accelerated since the actual conflict began. Plus, there have been fresh disruptions to shipping and supply chains as well as to agriculture production cycles in Ukraine and to some extent Russia, which will result in production shortfalls.

Let us look at how this has impacted various nations of late as per the inflation figures which have been released for several major economies over the past few days.

INDIA: Inflation Leaks Beyond the Commodity Categories...Likely to Impact Demand

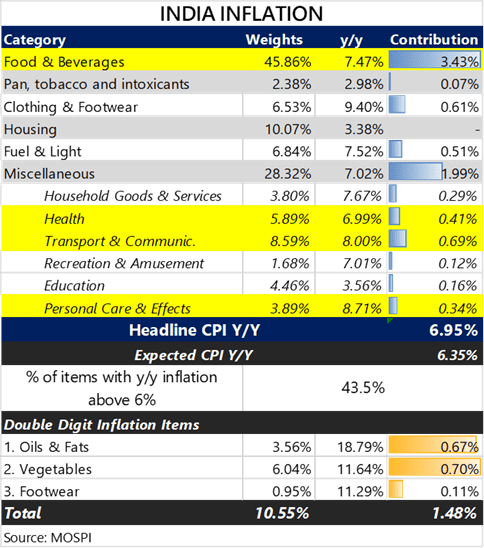

India's headline CPI hit 6.95% in March 2021 year on year (y/y), meaning over the same period last year. It is also up 0.96% month on month (m/m), i.e. over February 2022. This is the highest since November 2020.

Food & Beverages which account for almost half of the index jumped 7.5% y/y, thus contributing to more than 60% of the y/y acceleration in prices, led by double-digit increases in Oil & Fats (18.8% y/y) and Vegetables (11.6% y/y) which together account for about 9.4% of the index.

This isn't surprising given that the UN FAO’s global Food Price Index surged 13% m/m in March to a record high amidst constrained supplies (Russia-Ukraine war) and adverse weather conditions. As edible oil prices have risen 50-70% above pre-Covid levels, 24% of Indian households have cut down consumption while 67% are paying more for it by reducing spending and savings, shows a survey by LocalCircles.

However, clearly inflation has spread beyond the more directly explainable categories like edible oils. For example, the prices in the clothing and footwear category are up 9% year on year and even several services like health, transportation & communication, recreation etc. have seen 7-8% y/y inflation. All of this shows that inflation is becoming more entrenched.

This is in spite of the fact that the high Wholesale Price Index (WPI) inflation which has remained or about 13-14% for several months now has not really translated to that extent into higher consumer price inflation, as producers are still trying to hold back price increases given sluggish demand. However, given the recent runaway increase in commodity prices, they don't have much of a choice and consumer prices are beginning to rise for manufactured products as well.

As consumers have to pay more both for food as well as other daily use items, the discretionary spend is and will continue to get postponed.

The impact of fuel prices also is not visible in these numbers as those hikes have happened more recently. Fuel prices not only have a direct impact on the household budget but over time show up in higher prices of most goods and services as those have a transport component. This impact will be visible April onwards.

In our view, inflation is expected to accelerate in India over the next few months before it starts to moderate once the base effect kicks in (when the comparable period becomes a period of high inflation in the previous year). This will also impact the demand for a variety of goods, besides putting upward pressure on interest rates (already visible) and downward pressure on the Indian Rupee.

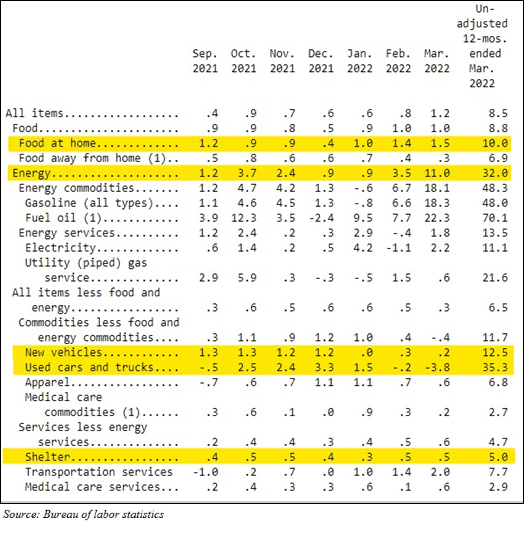

UNITED STATES: Non food and Fuel Inflation Begins to Moderate

US CPI y/y Actual 8.5% (Forecast 8.4%, Previous 7.9%)

US Core CPI (excluding food and fuel) y/y Actual 6.5% (Forecast 6.6%, Previous 6.4%)

US CPI m/m Actual 1.2% (Forecast 1.2%, Previous 0.8%)

US Core CPI m/m Actual 0.3% (Forecast 0.5%, Previous 0.5%)

Reaction: US treasury bonds rallied 6-10 bps as the curve bull steepened on softer than expected core CPI; the US dollar index (DXY) which measures the US Dollar against a basket of other currencies sold-off initially but settled 0.3% higher at 100.3, close to a 2-year high.

While headline inflation remained high, core Inflation, which excluded food and fuel, came in below consensus as Food at Home (1.5% m/m) and Energy (+11% m/m) were the main culprits.

Used Car & Trucks whose prices went through the roof in 2021 due to supply constraints for new vehicles, showed a decline in prices of 3.8% m/m which is a good sign.

However, the contribution of shelter inflation which measures housing costs, will remain sticky (+0.5% m/m, 5% y/y) due to lagged effects of soaring rents (refer to this paper for more details) and high weightage (33%) even as mortgage rates jump to 5.1%.

Overall, inflation may remain sticky at levels much higher than 2% (which has important ramifications on the monetary policy of the Fed and its rate hikes), there are signs that we are at or close to peak inflation in the US, given that price gains in food & energy as witnessed in the last 1-2 years are hardly sustainable without demand destruction and that base effects might also come in to play soon enough.

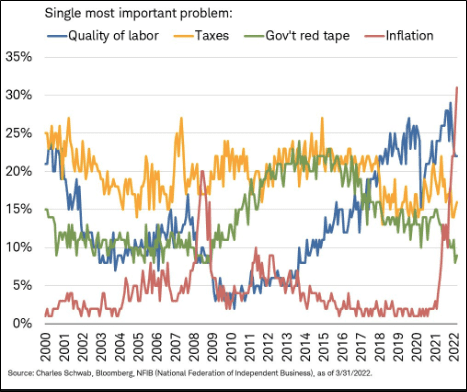

Elsewhere, according to the NFIB Small Business Survey released today, 31% of business owners identified inflation as their single most important problem, the biggest share since the Q1 of 1981, replacing worries about "labor quality" as the No.1 problem. The survey may be hinting at broader issues regarding the inflation pass-through capacity, given that inflation may not be a problem for businesses if growth/demand is also strong.

UNITED KINGDOM: Inflation Expectations Remain Worryingly High

UK CPI y/y Actual 7% (Forecast 6.7%, Previous 6.2%) -- 30-year high

UK CPI m/m Actual 1.1% (Forecast 0.8%, Previous 0.8%)

UK Core CPI, net of food and fuel, y/y Actual 5.7% (Forecast 5.3%, Previous 5.2%)

UK Core CPI, net of food and fuel, m/m Actual 0.9% (Forecast -, Previous 0.8%)

The headline and core CPI continue to be higher than expected with the Citi UK Inflation Surprise Index also hovering around its all-time-highs. Motor fuels prices surged 9.9% from February, the biggest increase in 31 years.

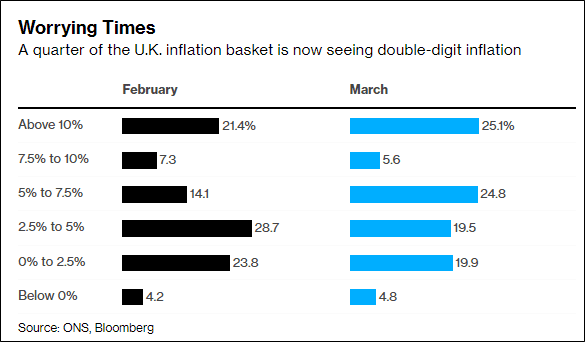

Market implied rates (meaning inflation expectations) such as those indicated by inflation swaps in the UK are priced for 9.6% inflation over the next 1 year (Note: In April, a 54% increase in energy bills is set to kick in, adding about 1.8 points to the headline rate) and gradually moving lower to average 5% average over the next 5 years. Longer term inflation expectations as indicated by 5-year forward 5-year inflation rate have been trending higher for more than year and currently sit at ~4% i.e. double the Bank of England’s target of 2%. The breadth and severity of the inflation has accelerated to worrying levels indeed (see image below). Large retailers such as Tesco have already issued profit warnings on the back of this.

The table above gives the percentage of items from the inflation calculation categories that fall in each inflation band. Thus 25% of the categories for which prices are measured, saw a 10% plus increase in inflation.

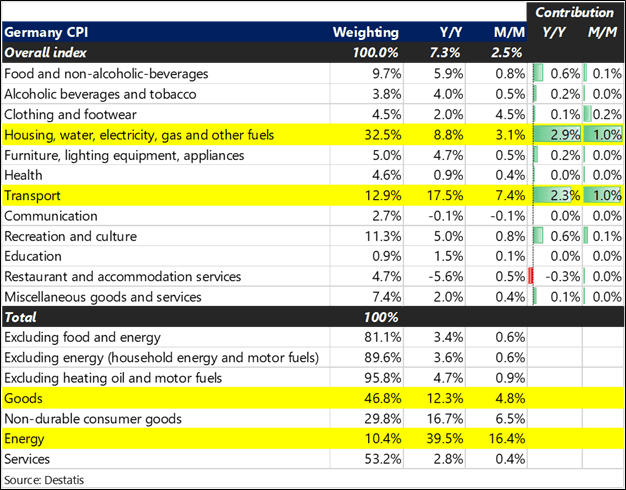

GERMANY: Headed into Historically High Inflation

German headline CPI comes in at 7.3% y/y the highest since 1981 while the m/m print of 2.5% is the largest since October 1952 - led primarily by food and energy (ex-food/energy is 0.6% m/m and 3.4% y/y). Goods inflation continues to dominate at 4.8% m/m and 12.3% y/y vs. 0.4% m/m and 2.8% y/y for services. Meanwhile, WPI registers another record peak of 22.6% y/y and 6.9% m/m.

Germany has traditionally been an inflation hawk due to the country's bout with hyperinflation almost 100 years back.

However this time it held back on raising interest rates for a long time but obviously such historic levels of inflation have now put pressure on Bond yields in the EU as well.

Here's how 10 year Treasury bond yields have moved across the EU from January 1 till date (bps stands for basis points 100 basis points = 1 percent points)

Germany: +90bps to 0.79%

France: +107bps to 1.27%

Spain: +110bps to 1.72%

Italy: +120bps to 2.39%

UK: +83bps to 1.82%

Poland: +240bps to 5.90%

Hungary: +227bps to 6.67%

Czech Republic: +110bps to 4.10%

Across the world, inflation will continue to be the most watched macro variable this year that will, in turn, be the key factor driving interest rate moves by Central Banks from the RBI to the Fed. The rate changes in turn are big determinants of valuations in both equity and fixed income markets. This will be the space to watch.

From the desk of Devina Mehra

If you want any help at all in your wealth creation journey, in managing your Investments, just drop us a line via this link and we will be right by your side as your wealth advisor, super quick!

Or WhatsApp us on +91 88501 69753

Chat soon!

Economists Think Dollar's Fall May Explain the Recent ‘Rally’ by Steve Liesman

Einstein taught us about relativity in nature. Now come Devina Mehra and Shankar Sharma of First Global to teach us about relativity in financial markets -- and raise some serious questions about just what is driving stock prices.

First Global reports are quite credible and, on occasion, more than that.

What prompts this mention is Intel's earnings report and the fact that First Global has had a pretty good bead on the company and its stock.

AMD up again following First Global upgrade to ‘buy’ (AMD) By Tomi Kilgore

Analyst Kuldeep Koul at First Global upgraded Advanced Micro Devices (AMD) to "buy" from "outperform," given the "exceptional traction" that the chipmaker's Opteron line of processors has been able to get.

Baidu Climbs on First Global’s ‘Outperform’ Outlook

Baidu Inc., the operator of China’s most-used Internet search engine, rose to the highest price in two weeks after First Global rated the shares “outperform? in new coverage.

Personality counts: Walmart's frugal, but Target charms

"It's better to take a slight hit on [profit] margins and keep on moving and inventing," says First Global Securities. And at least for now, Target is inventing in a way that appeals to consumers with money to spend.

Dead Batteries

At 11 times trailing earnings, Energizer is cheaper; Gillette's multiple is 25. But cheaper doesn't mean better, says First Global.

Bipinchandra Dugam @bipinchandra90

@devinamehra @firtglobalsec

invested in both GFF-GTS and Super I50. Thank you very much for such wonderful investing experience with completely new approach. In my 15years of investing first product I felt which close to what customer want.

Shishir Kapadia @shishirkapadia1

@firstglobalsec @devinamehra

by far you are the best, I have not come across transparency, acumen, global expertise, exposure, protection of capital, delivering return from any fund/ fund managers. Invested very small size in 3 products will keep on increasing it over the period

Piyush Bhargava @PiyushB88762654

@devinamehra @firstglobalsec

Thanks you team FG specially Devina, my investment doubled in less than 3 years in SDPB As a investors & PMS distributor of your product looking to have a long-term relationship with the company.

@KarmathNaveen the person with whom I always interact

Sumeet Goel @GoelSumeet

Very happy & relaxed to be invested with first global pms

Shishir Kapadia@shishirkapadia1

Congratulations on super performance, above all transparency and systematic process are unmatchable.

One must opt this, if person consider him/her self as an investor. Very happy to be part of this since invested. FG has managed worst year (ie 2022) so efficiently and skillfully.

SY @SachinY95185924

With so much of volatility in the market, risk management is very important part & considering that FG is doing awesome work!!! Kudos to you Chief

Amit Shukla @amitTalksHere

Truly outstanding. As a retail subscriber to #fghum #smallcase, I can vouch for the Nifty beating returns (8% vs 3%) in last 1 year. Keep up the awesome work @firstglobalsec

We can load above testimonials on site as a scroller, and just below that we can add a section for compliments . Below tweets are comments and praises are related to our content, performance and some our direct compliments to you.

ADIT PATEL @ADITPAT11226924

Good team...

Special mention @KarmathNaveen .. he is soo helpful anytime of the day or night..

Hindustani @highmettle

Bought Peace with FG-Hum.Moving all funds from DIY investing to well managed and diversified PF at low cost.

It has doubled almost, excellent pick.Every small investor must invest in her FG-HUM Smallcase.

Suresh Nair @Suresh_Nair_23

I have 8 small cases and your has been the most rewarding ones .. thank you Devina.

Sayed Masood @SayedM375

There is absolutely no doubt that she is one of the best investors of India in modern times but more importantly, she shares the most sincere and sane advice with retail investors.

SY @SachinY95185924

Wow Superb Returns🔥 Congratulations Chief for being Number 1 among all PMS!!!

You are one of the sharpest mind in Global Stock Market

AnupamM @moitraanupam

Congratulations Devina, results talk in itself!

Abhishek @simplyabhi21

Congratulations ma’am @devinamehra ! The consistency you have in maintaining the top rank position is outstanding! 👏

Mihir Shah @Mihir41Shah

We are learning More about markets (& Life ) thanks to U than we learnt in our Professional courses.A BIg Thank You, Wish all get Teachers Like You!!

Sumit Sharma @MediaSumit

"The ability to be comfortable with being outside consensus is a superpower in investing...and in life." Devina ji hits the nail on its head!

Majid Ahamed @MajidAhamed1

Congratulations @devinamehra mam! All the best for long term returns as well.

Vinay Kumar @VinayKu05949123

This is the wonderful session I have ever attended till date. One of the most fruitful hour of my life. Devina madam, ur clarity on financial mkts is simply superb.The way u portray the facts supported by "data" about stock mkts is really astonishing.I will listen again.Thanks.

VIJAY @drippingashes

I loved to read your journey, insight and philosophy. It's a pleasure to read and know of your takes on market and life.

MNC🏹 @Focus_SME

Check & follow @devinamehra's timeline for lots of post debunking such rosy stories. Also, she gives amazing 🤩 sector directions/hints.

KLN Murthy @KLNMurthy2016

Good actionable insights, great article!

Suresh Nair @gkumarsuresh

Devina Madam is simply terrific... good knowledge, straight and simple thinking.

Very difficult to emulate such traits. I listen her past interviews from youtube.

Respect...!!!!

DD @AliensDelight

One of the brightest minds in the world of finance :)

Radhakrishnan Chonat @RCxNair

📣 Calling all investors! Just had an incredible interview with @devinamehra, Chairperson and MD of First Global. We discussed the importance of global diversification, effective asset allocation, and the risks of sitting on the sidelines. Trust me, you don't want to miss this!

siddarthmohta @siddarthmohta

Excellent performance. Flexibility is the key as you have mentioned it earlier also. Cannot have finite rules for infinite mkt opportunities.

Boom (বুম)@Booombaastic

To be honest, the insights which Devina madam brings in is very enriching..have learnt a lot from them...

Himanssh Kukreja @Himansh02428907

One of the most accurate analysts :)

I always look forward to you interviews mam

Abhijeet Deshpande @AbhijeetD2018

Madam, It is always a treat to read your insight, not only on business but on other topics also!!

Dada.AI @dada_on_twit

Thanks for this wisdom ma'am. Always love hearing your thoughts on everything equity. :-)

adil @zinndadil

Excellent points!

Can clearly feel this thread is a product of marination of many books and years of experience. 👍

Kamal thakur @Kamalgt10

Superb !!

Your knowledge, analysis & articulation is simply great 👍

Tanay @Tanay36232730

Follower on Twitter and Subsciber on YouTube of First Global, really helping me in my investment desicion. Thanks

Copyright 2019, All Rights Reserved. Developed By : Hvantage Technologies Inc. Maintain By : Aarav Infotech